ABOUT

About Us

Our Team

Contact Us

WHY JOIN REIP?

Why Join REIP?

Become a Member

MEDIA

REIP in the News

Behind the Numbers Podcast

Inside Real Estate

REIP NEXUS

Become a member

ABOUT

About Us

Our Team

Contact Us

WHY JOIN REIP?

Why Join REIP?

Become a Member

MEDIA

REIP in the News

Behind the Numbers Podcast

Inside Real Estate

REIP NEXUS

Become a member

ABOUT

About Us

Our Team

Contact Us

WHY JOIN REIP?

Why Join REIP?

Become a Member

MEDIA

REIP in the News

Behind the Numbers Podcast

Inside Real Estate

REIP NEXUS

ABOUT

About Us

Our Team

Contact Us

WHY JOIN REIP?

Why Join REIP?

Become a Member

MEDIA

REIP in the News

Behind the Numbers Podcast

Inside Real Estate

REIP NEXUS

Industry

Home

Archive by Category "Industry"

Category: Industry

07

Jul

Industry

What is the RiSE Initiative?

Read More

27

Jun

Industry

The two ‘Sliding Door’ choices for Property Managers: Ignore wellbeing… or embrace it and lift performance?

Read More

13

Jun

Industry

National Recovery Underway?

Read More

30

May

Industry

Gold Coast Market Rebounds Strongly In Past Quarter

Read More

16

May

Industry

At A Crossroads: Is This A Turning Point?

Read More

02

May

Industry

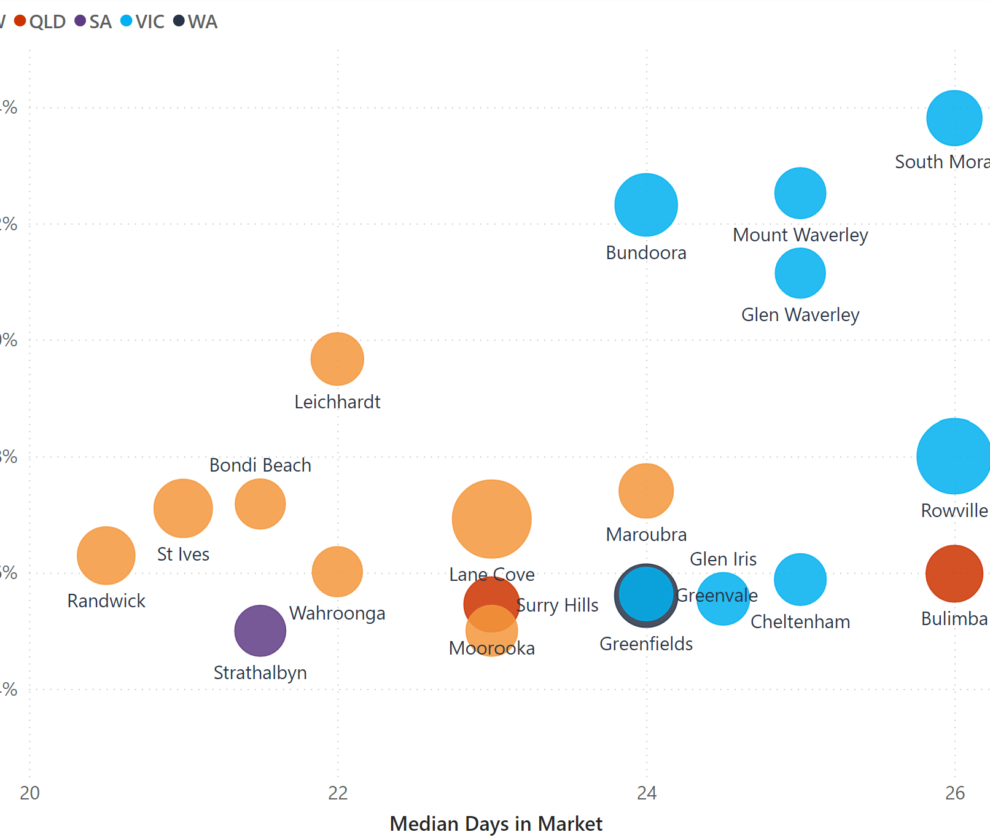

The Top Twenty Hottest Suburbs For Jan-Apr 2023

Read More

18

Apr

Industry

Victoria still the auction capital

Read More

03

Apr

Industry

Apartments making a comeback amidst strong rental investments in Perth

Read More

21

Mar

Industry

Blacktown City Shines with Thriving Population and Sustainable Housing

Read More

07

Mar

Industry

Western Australia and South Australia holding strong amid national challenges

Read More

1

2

3

BACK TO TOP